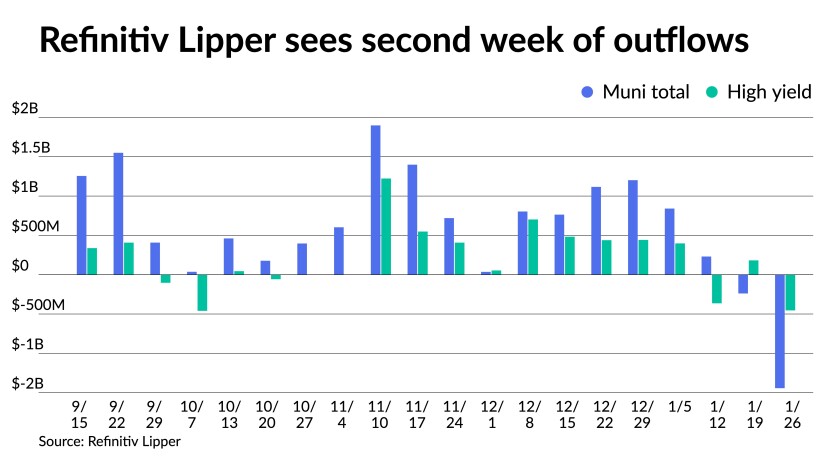

Municipals were hit hard Thursday with up to 10 basis point cuts on the short end, but the damage was felt across the curve. Refinitiv Lipper reported $1.4 billion of outflows, the largest since 2020, while the U.S. Treasury curve flattened further and equities ended in the red again.

Triple-A yields rose by five to 10 basis points while Treasuries saw the short end rise by four basis points while the long bond fell by eight. Ratios rose on the day’s moves with the municipal to UST five-year at 67%, 80% in 10 and 88% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 67%, the 10 at 83% and the 30 at 89%.

Municipals are looking at record-breaking losses in January will undoubtedly define the first month of the new year, said Jeffrey Lipton, head of municipal credit and market strategy and municipal capital markets at Oppenheimer & Co LLC. As a result, investors will likely adopt a more cautious stance going forward.

Returns are deep in the red with the Bloomberg Municipal Index at negative 1.85%, while high-yield sits at negative 1.81%. Taxable munis saw losses of 2.64% so far this year and the Municipal Impact Index has seen losses of 2.30%.Understanding credit ratingsMoody’s Investors Service is a leading global provider of credit ratings, research and risk analysisPARTNER INSIGHTS

MOODY’S

The path to higher interest rates will undoubtedly test munis’ boundaries and resiliency, but Lipton said he is confident the market’s resiliency will be preserved by the continuation of tax efficiency, above-average credit quality, defensive qualities in a rising-rate environment and diversification attributes.

“Our caution, however, surrounds the very real possibility that market participants are setting their expectations too high,” he said.

Munis have been hit by a wave of fixed-income outflows, with investors taking money out of municipal bond mutual funds, snapping a 45-week streak of positive flows and highlighting steep exchange-traded fund and high-yield redemptions.

While bid-wanted activity did not have a significant impact on the muni market in 2021, Bloomberg reports that bid lists in January saw the most secondary offers since April 2020, Lipton noted. Indeed, bid lists were high again Thursday and hit $1.098 billion on Wednesday after $1.202 billion Tuesday.

“Given the rate volatility that will likely characterize fixed income throughout 2022, munis can be expected to more closely follow the directional movements of UST yields during much of the year,” Lipton said. “However, there will likely be breakaway points as demand is expected to hold in and this could become more pronounced should the higher tax narrative reemerge.”

Price discovery will most likely take hold when market players analyze a new trading range and move through this more volatile time, Lipton said.

Lipton doesn’t expect a protracted period of negative flows at this time but may expect more intermittent outflows.

Although cash is available, he said there will certainly be a cautious attitude toward its future use.

For the time being, Lipton predicts mildly positive muni returns in 2022, with outperformance above U.S. Treasury and investment-grade corporates. However, there will very certainly be stronger headwinds on the way there, he said.

Lipton said the performance of muni high-yield this year will most likely be determined by the future pattern of investment grade spread relationships, and if spreads manage to remain reasonably compressed, high-yield performance could book another notable year, and even the lower spectrum of investment grade can perform reasonably well.

In the primary Thursday, Citigroup Global Markets priced for Ohio Housing Finance Agency (Aaa///) $195 million of social non-alternative minimum tax residential mortgage revenue bonds. Bonds maturing in 9/2022 with a 0.45% coupon at par, 5s of 3/2027 at 1.37%, 5s of 9/2027 at 1.43%, 2.25s of 2/2032 at par, 2.25s of 9/2032 at par, 2.45s of 9/2037 at par, 2.7s of 9/2042 at par, 2.85s of 9/2046 at par and 3.25s of 9/2052 at 1.74%, callable 9/1/2031.

FHN Financial Capital Markets priced for Forney Independent School District, Texas (/AAA//) $160.665 million of unlimited tax school bonds, Series 2022A. Bonds maturing in 2033 with a 4% coupon yields 1.8%, 3s of 2037 at 2.16%, 3s of 2042 at 2.31%, 4s of 2042 at 2.08%, 2.75s of 2048 at 2.83% and 2.875s of 2052 at 2.88%, callable 8/15/2031.

In the competitive market, Spartanburg County School District #5, South Carolina, (Aa1/AA//) sold sell $100 million of general obligation bonds, Series 2022, to J.P. Morgan Securities. Bonds maturing in 3/2023 with a 5% coupon yields 0.55%, 5s of 2027 at 1.15%, 5s of 2032 at 1.5%, 3s of 2037 at 1.99%, 2.625s of 2042 at 2.63% and 2.75s of 2046 at 2.82%, callable 3/1/2032.

Mutual funds see large outflows

In the week ended Jan. 26, weekly reporting tax-exempt mutual funds saw $1.432 billion of outflows, Refinitiv Lipper said Thursday. It followed an outflow of $238.92 in the previous week.

Exchange-traded muni funds reported outflows of $209.020 million, after inflows of $56.463 million in the previous week. Ex-ETFs, muni funds saw outflows of $1.223 billion after $295.389 of outflows in the prior week.

The four-week moving average fell to negative $149.964 million from $508.754 million in the previous week.

Long-term muni bond funds had outflows of $760.347 million in the latest week after inflows of $426.196 million in the previous week. Intermediate-term funds had outflows of $157.818 million after $70.812 million of outflows in the prior week.

National funds had outflows of $1.291 billion after $312.876 million of outflows the previous week while high-yield muni funds reported $453.999 million of outflows after inflows of $182.035 million the week prior.

Informa: Money market muni funds fall

Tax-exempt municipal money market fund assets decreased their total by $1.25 billion, bringing their total to $86.2 billion for the week ending Jan. 25, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 150 tax-free and municipal money-market funds remained at 0.01%.

Taxable money-fund assets rose $31.74 billion, bringing total net assets to $4.506 trillion in the week ended Jan. 25. The average seven-day simple yield for the 780 taxable reporting funds was steady at 0.01% from a week prior.

Secondary trading

Florida Board of Education 5s of 2023 at 0.6%. Connecticut 5s of 2024 at 1.03%. Washington 5s of 2024 at 0.9%.

DASNY 5s of 2027 at 1.32%. Georgia 5s of 2029 at 1.36%. California 5s of 2029 at 1.53%.

District of Columbia 5s of 2034 at 1.89%. Ohio Water Development Authority 5s of 2034 at 1.54%. Michigan Finance Authority 5s of 2035 at 1.63%.

New York City Transitional Finance Authority 5s of 2047 at 2.2%. New York City 5s of 2047 at 2.29%. Los Angeles Department of Water and Power 5s of 2051 at 2.11%.

AAA scales

Refinitiv MMD’s scale saw six to 10 point cuts at the 3 p.m. read: the one-year at 0.53% (+10) and 0.79% (+10) in two years. The five-year at 1.11% (+8), the 10-year at 1.45% (+8) and the 30-year at 1.85% (+6).

The ICE municipal yield curve was cut five to seven basis points: 0.53% (+7) in 2023 and 0.83% (+7) in 2024. The five-year at 1.12% (+7), the 10-year was at 1.49% (+6) and the 30-year yield was at 1.87% (+5) in a 4 p.m. read.

The IHS Markit municipal curve was cut one to two basis points: 0.55% (+10) in 2023 and 0.77% (+10) in 2024. The five-year at 1.09% (+7), the 10-year at 1.43% (+7) and the 30-year at 1.87% (+7) at a 4 p.m. read.

Bloomberg BVAL was cut six to 11 basis points: 0.59% (+9) in 2023 and 0.78% (+10) in 2024. The five-year at 1.02% (+10), the 10-year at 1.46% (+8) and the 30-year at 1.85% (+6) at a 4 p.m. read.

Treasuries flattened and equities ended in the red.

The two-year UST was yielding 1.191%, the five-year was yielding 1.662%, the 10-year yielding 1.807%, the 20-year at 2.17% and the 30-year Treasury was yielding 2.09% at the close. The Dow Jones Industrial Average lost 7 points or 0.02%, the S&P was down 0.54% while the Nasdaq gained 1.40% at the close.

FOMC redux

Life during a pandemic isn’t easy and the Federal Reserve will have a difficult time navigating the economy to a safe landing, analysts said.

“The Fed needs to distinguish the signal from the noise,” said Ron Temple, head of U.S. equities at Lazard Asset Management. “Some investors think the Fed is behind the curve. Others are fearful of the inevitable withdrawal of a tsunami of easy money.”

With growth deceleration, inflation believed to be near its peak, and workers expected to reenter the workforce later in the year, pushing up the unemployment level, he said, “the best option is to tighten policy marginally and retain flexibility, recognizing it is easier to reduce inflation caused by overheated demand, than to correct for excessive hawkishness.”

But “the Fed has a potentially difficult juggling act ahead,” said Ned Davis Research Chief Global Macro Strategist Joe Kalish, and Senior U.S. Economist Veneta Dimitrova. “It needs to bring inflation down without sending the economy into recession or creating financial instability. As a result, it needs to prepare for a wide range of outcomes.”

And while the Fed now has experience with quantitative tightening, the circumstances are different. Inflation is higher, the unemployment rate is lower and the balance sheet is “much larger” than the last time the Fed stopped buying assets to fuel the economy.

However, they noted, “the Fed is much better prepared for asset reductions. It has a permanent Standing Repo Facility (SRF) to address any unforeseen liquidity needs and it has an Overnight Reverse Repo Facility (RRP) to help absorb excess cash.”

Before the announcement, “the markets had been reacting in a risk-off manner,” said John Farawell, managing director and head of municipal trading at Roosevelt & Cross. “The performance of the Treasury and equity markets seem to perceive a less accommodate Fed.”

The Fed has already failed on inflation, said deVere Group CEO Nigel Green, and has admitted that it may not decline to its 2% target anytime soon. “Why, then, did the world’s most powerful central bank not act sooner to stem this off quicker?” he asked. “This grand scale inaction must be the biggest miscalculation in the Fed’s history.”

While the market has priced in at least four rate hikes this year, “I would urge the Fed not to fail on inflation again by hitting the brakes with too many rate hikes,” Green said. “The excess money in the system will come out fast. There’s a real risk that numerous interest rate hikes would cause a recession and may not even slow inflation as the soaring prices are triggered by supply chain issues which the Fed’s hikes will not solve.”

But rate hikes alone won’t cool demand in inflation-causing sectors including homes and autos, said Jake Remley, senior portfolio manager at Income Research + Management. “The rationale is that the front end has only so much influence over consumer borrowing rates.”

Balance sheet reduction will also be needed, he said, suggesting they allow mortgage-backed securities “to runoff without the corresponding monthly reinvestment.”

And, rate hikes and QT can be done together without causing “sustained volatility,” Remley said, provided the Fed “can be clearer” about their intentions.

Not that the Fed should be concerned about “some market disruption,” given the accommodative nature of current financial conditions, he said. In fact, Remley added, the panel has “some wiggle room” if it wants to raise rates 50 basis points in March.

But Jay Hatfield, chief investment officer at InfraCap Equity Income ETF, noted, “Investors are fearful of a repeat of 2018, where the Fed was both increasing rates and reducing the balance sheet and the market was down over 7% for the year and the economy almost went into recession.”

Issuing the balance sheet reduction principles separately, “was viewed by the market as a hawkish sign that the Fed may rapidly decrease the balance sheet,” he said. “Also, the statement focused on mortgage security reduction, which is more restrictive than equal reduction.”

But, Federal Reserve Board Chair Jerome Powell suggested the FOMC will discuss the balance sheet at the next meeting or two, noted David Page, head of macroeconomic research at AXA Investment Managers, which could lead to a June announcement about balance sheet reduction.

“If QT does not dampen activity quickly enough,” he said, “the Fed may consider a quicker pace of rate hikes, more quickly reaching and plausibly exceeding its current 2.5% terminal rate estimate.” This will make March’s Summary of Economic Projections “revealing,” Page said, perhaps signaling more than four rate hikes in 2022.

The post-meeting statement was exactly as the markets expected, said Marvin Loh, senior macro strategist at State Street Global Markets. But when Powell wouldn’t elaborate at his press conference, it left “the door open for a more hawkish interpretation.”

Powell’s assertion the Fed needs to be “nimble and flexible,” Loh said, suggested to investors “the possibility of a more aggressive start in March (50 bps), potential hikes every meeting and a higher terminal rate,” he said, noting, “flexibility also means a slower pace, although inflation concerns are pushing the market to expect more rather than less.”

The market interpreted Powell’s remarks as hawkish, and Loh said, “we suspect that this tone will continue until we get further clarity on inflation and possible growth headwinds in coming releases.”

Thursday’s data suggested a stronger economy. Gross domestic product rose 6.9% in the fourth quarter, topping expectations of a 5.4% gain.

“Two items of note stick out in this preliminary read on economic growth in the fourth quarter of 2021: supply-chain issues challenged many sectors of the economy, and inflation is running well above the Federal Reserve’s target,” said Mortgage Bankers Association SVP and Chief Economist Mike Fratantoni.

Most of the gain came from “a significant jump in business spending on inventories,” he said. “This likely reflects the ongoing challenges so many sectors of the economy have had with supply-chain constraints. Some companies may move to higher steady state inventory levels going forward to prevent the disruption that supply-chain issues have caused, and this ongoing restocking behavior could continue to lead to above trend growth in 2022.”

But don’t get used to that type of growth said Wells Fargo Securities Senior Economist Tim Quinlan and Economist Shannon Seery. “Tthe details behind the better-than-expected headline point to a slowing in spending and a back-up in inventories. Without the boost from inventories, GDP would have been just 2.0% in Q4.”

Sustaining economic growth in the next year or two “not just in the absence of fiscal policy, but in the face of tightening monetary policy” will be challenging, they said.

And the first quarter could see much slower growth, said James Knightley, ING chief international economist. “The Omicron variant hit activity hard in December and this has carried through into January, setting us up for a soft 1Q 2022 GDP figure.”

Also released Thursday, durable goods orders fell 0.9% in December, more than the 0.5% drop expected by economists polled by IFR Markets. Excluding transportation orders grew 0.4%.

Initial jobless claims dropped to 260,000 in the week ended Jan.22 from 290,000 a week earlier.

“How the job market and the broader economy react both to the prospect and the reality of rising interest rates this year will be key questions of interest to individuals, households, and enterprises alike,” said Mark Hamrick, senior economic analyst at Bankrate. “All have been given fair warning that rising rates are ahead.”

Original Source: https://www.bondbuyer.com/news/muni-rout-continues-outflows-hit-1-4-billion