Municipals were better across the curve with the largest bumps out long Wednesday, moving the 30-year down 11 basis points in two days, while U.S. Treasuries were slightly better and equities saw modest gains.

Triple-A benchmarks saw yields fall one to seven basis points while UST were better by one to two basis points. Ratios fell slightly as a result. The municipal to UST ratio five-year was at 74%, 82% in 10 and 88% in 30, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the five at 72%, the 10 at 84% and the 30 at 87%.

Buyers appeared to return to the market the past two sessions after the January correction moved yields and ratios higher. Secondary trading was up again on Wednesday and new deals were well-received.

Secondary trading showed clear moves to lower yields, particularly out long. Block trading of Los Angeles Department of Water and Power 5s of 2041 at 1.80% versus 1.93% Tuesday and 1.97% Friday. Washington 5s of 2043 at 1.85%-1.84% versus 2.03%-2.02% Monday.Bitvore for Munis: Make better decisions faster with AI powered solutionsGain early warnings on material changes in muni obligors. Bitvore analyzes unstructured data from 60k+ unique sources of data and extracts valuable risk,…PARTNER INSIGHTS FROM BITVORE

Further out, LA DWP 5s of 2046 at 1.97%-1.93% versus 2.01%-2.00% Tuesday. New York City Transitional Finance Authority 5s of 2047 at 2.14%-2.13% versus 2.24%-2.18% Tuesday. New York City waters 5s of 2048 at 2.09%-2.08% versus 2.21%-2.18% Thursday. LA DWP 5s of 2051 at 2.05%-1.98% versus 2.19% Friday.

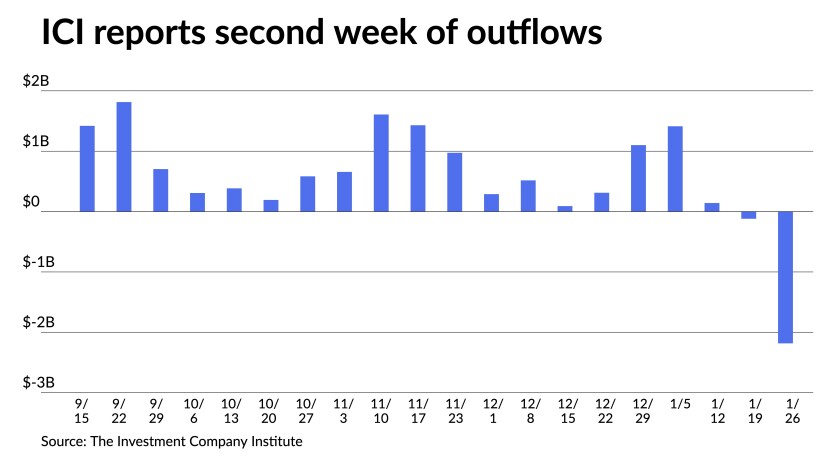

The Investment Company Institute on Wednesday reported $2.183 billion of outflows from municipal bond mutual funds in the week ending Jan. 26, from $119 million of outflows in the previous week.

It marked the largest reported outflows since 2020 and the second week of outflows after 45 straight weeks of positive flows into the long-term funds. Exchange-traded funds also saw outflows at $523 million after $1 million of inflows the previous week.

While higher interest rates aided a record dismal January for municipal bonds, other factors exacerbated the losses, said Eric Kazatsky, head of municipal strategy for Bloomberg Intelligence.

“Among these is dealers’ heavy exposure to munis at the end of 2021, hoping for a ‘January effect’ that never came,” he said. “Also, recent tax-law changes and low rates have reshaped how bonds are sold, leaving holders less insulated from a sharp rate backup.”

The number of bonds sold with coupons of 5% or greater is at an all-time low, while those with coupons of zero to 3% are at an all-time high, he said.

This trend has escalated since 2017 when premium coupons accounted for 55% of the market. By 2021, he said that figure had dropped to around 31%. Sub-3% discounts accounted for 10% of the market in 2017, while they accounted for almost 26% last year.

Technical, rather than fundamental, dynamics have largely driven recent market moves, according to Morgan Stanley strategists.

“Following the early impacts of the pandemic, municipal bond demand accelerated due to the receipt of healthy federal stimulus, the temporary instatement of the [Federal Reserve’s] Municipal Liquidity Facility, prodigious market liquidity, a firm interest rate backdrop and anticipations for higher federal, state and local income taxes,” they said.

In February 2021, relative-value ratios broke all-time highs for strength — just under 55% on the 10-year triple-A benchmark — thanks to this low-supply/healthy-demand technical imbalance.

When a healthy municipal bond market is combined with a weak U.S. Treasury background, Morgan Stanley strategists said tax-exempt securities have no alternative but to follow Treasuries’ price behavior.

If Treasury prices fall dramatically, causing interest rates to increase, but municipals remain strong, they said crossover investors — who are frequently more agile and not buy-and-hold participants— will likely sell tax-exempt bonds over taxable ones. For decades, they said this technical link has assisted in balancing dislocations between the two markets. Municipal bond mutual fund flows frequently demonstrate sluggish reactions to larger interest rate fluctuations, which helps to fix imbalances.

“This technical response has occurred and, since, has been further exacerbated by the reality that many lower-coupon municipals have been repriced to longer final maturities, instead of shorter call dates,” they said.

In the primary market Wednesday, Goldman Sachs & Co. priced for the New York Liberty Development Corporation $449.19 million of green tax-exempt liberty revenue refunding bonds, Series 2022A. The first tranche, $355.195 million of Class 1 (Aaa///) saw bonds maturing in 9/2043 with a 3% coupon at par and 3.125s of 2050 at par, callable 3/15/2030.

The second tranche, $58.8 million of Class 2 (Aa3///) saw bonds maturing 9/2052 with a 3.25% coupon at par, callable 3/15/2030.

The third tranche, $35.195 million of Class 3 (A2///) saw bonds maturing 9/2052 with a 3.5% coupon at par, callable 3/15/2030.

Siebert Williams Shank & Co. priced and repriced Broward County, Florida (Aa1/AA+///) $199.265 million of water and sewer utility revenue bonds, Series A, with up to 12 basis points bumps. Bonds maturing in 10/2028 with a 5% coupon yield 1.51%, 5s of 2032 at 1.75% (-2), 5s of 2037 at 1.91% (-5), 4s of 2042 at 2.15% (-10) and 4s of 2047 at 2.38% (-12), callable 10/1/2031.

BofA Securities priced for Jacksonville, Florida (/AA/AA-/AA) $121.155 million of forward delivery special revenue refunding bonds, Series 2022A. Bonds maturing 10/2023 with a 5% coupon yield 1.22%, 5s of 2027 at 1.86% and 5s of 2032 at 2.16%.

Jefferies preliminary priced for Massachusetts State College Building Authority (Aa2/AA-//) $108.05 million of project and refunding revenue bonds, Series 2022A. Bonds maturing in 5/2023 with a 5% coupon yield 0.74%, 5s of 2027 at 1.45%, 5s of 2032 at 1.77%, 4s of 2037 at 2.13%, 4s of 2042 at 2.25%, 4s of 2047 at 2.36% and 4s of 2052 at 2.41%, callable 5/1/2032.

Informa: Money market muni funds fall

Tax-exempt municipal money market fund assets fell by $471.2 million, bringing their total to $85.73 billion for the week ending Jan. 31, according to the Money Fund Report, a publication of Informa Financial Intelligence.

The average seven-day simple yield for the 150 tax-free and municipal money-market funds remained at 0.01%.

Taxable money-fund assets lost $15.74 billion, bringing total net assets to $4.49 trillion in the week ended Jan. 18. The average seven-day simple yield for the 780 taxable reporting funds was steady at 0.01% from a week prior.

Secondary trading

New York City Transitional Finance Authority 5s of 2023 at 0.80%. DASNY sales tax 5s of 2024 at 0.95% versus 1.03% Tuesday. New York City 5s of 2024 at 1.00%.

Alexandria, Virginia 5s of 2027 at 1.22%. Minnesota 5s of 2028 at 1.34%-1.32% versus 1.38% Tuesday. District of Columbia income tax 5s of 2029 at 1.49%-1.48%.

Washington 5s of 2041 at 1.55% versus 1.60% Tuesday. Baltimore County 5s of 2031 at 1.51% versus 1.57% Tuesday and 1.62%-1.60% Monday. Fairfax County, Virginia 4s of 2031 at 1.57% versus 1.62% Tuesday.

California 5s of 2032 at 1.56%-1.55% versus 1.73%-1.71% Monday. Maryland 5s of 2033 at 1.53% versus 1.57% Tuesday. Connecticut 5s of 2033 at 1.77%-1.76%.

Los Angeles Department of Water and Power 5s of 2037 at 1.71% versus 1.85%-1.84% Tuesday. California 5s of 2037 at 1.76%-1.68% versus 1.77% Tuesday. LA DWP 5s of 2041 at 1.80% versus 1.93% Tuesday and 1.97% Friday. California 5s of 2041 at 1.83%-1.81%. Washington 5s of 2043 at 1.85%-1.84% versus 2.03%-2.02% Monday.

Pennsylvania Higher Educational Facilities Authority UPenn 5s of 2044 at 2.17%-2.16%. Triborough Bridge and Tunnel 5s of 2051 at 2.12% versus 2.18% Thursday.

AAA scales

Refinitiv MMD’s scale was bumped one to seven basis points the 3 p.m. read: the one-year at 0.63% (-1) and 0.90% (-1) in two years. The five-year at 1.19% (-5), the 10-year at 1.45% (-5) and the 30-year at 1.84% (-7).

The ICE municipal yield curve saw one to six basis point bumps: 0.60% (-1) in 2023 and 0.91% (-2) in 2024. The five-year at 1.16% (-3), the 10-year was at 1.50% (-5) and the 30-year yield was at 1.84% (-5) in a 4 p.m. read.

The IHS Markit municipal curve was little changed on the short end and bumped out longer: 0.65% in 2023 and 0.88% in 2024 (both unch). The five-year at 1.21%, the 10-year at 1.45% (-7) and the 30-year at 1.87% (-7) at a 4 p.m. read.

Bloomberg BVAL was bumped one to six basis points: 0.65% (-1) in 2023 and 0.87% (-1) in 2024. The five-year at 1.21% (unch), the 10-year at 1.46% (-6) and the 30-year at 1.85% (-6) at a 4 p.m. read.

Treasuries were steady and equities ended in the black.

The two-year UST was yielding 1.172%, the five-year was yielding 1.627%, the 10-year yielding 1.797%, the 20-year at 2.187% and the 30-year Treasury was yielding 2.120% at the close. The Dow Jones Industrial Average gained 224 points or 0.63%, the S&P was up 0.94% while the Nasdaq gained 0.34% at the close.

Labor blip? No worries

Employment is in the spotlight this week, but the focus on labor has faded in favor of inflation, especially with Omicron expected to wreak havoc on January’s jobs data.

Given this explanation, the Federal Reserve will likely ignore the weakness shown in Wednesday’s ADP report, which showed 301,000 private-sector jobs lost in January, unless the sector fails to rebound in the next two months, analysts said.

“It’s hard to know exactly how to interpret” the report, said Morning Consult Chief Economist John Leer. “ADP’s payroll forecasts in November and December were significantly larger than the [Bureau of Labor Statistic’s] reported numbers,” he said.

If the trend holds, Leer said, the nonfarm payrolls could see large losses. “On the other hand, if ADP’s January forecast reflects some sort of offsetting correction to make up for the overly optimistic forecasts in November and December, the BLS print on Friday may not be that bad.”

But, he believes “Friday’s jobs report itself is likely to be discouraging,” but only “a short-term setback in an otherwise impressive jobs recovery.”

Therefore, it would take “several consecutive negative monthly prints to delay the upward path of interest rates that markets are expecting,” Leer said.

With economists polled by IFR expecting ADP to show a 208,000 gain in employment, the decline “was a surprise,” said John Farawell, managing director and head of municipal trading at Roosevelt & Cross. But it “can be explained by the Omicron variant and its prevalence in the labor force.”

Looking ahead to Friday’s report, it “will likely reflect an economy grappling with the less-than-optimal mix of the Omicron variant wave and worker shortages,” said Mark Hamrick, senior economic analyst at Bankrate. The jobs added total “could be the lowest in a year and possibly even [show] a decline,” he said.

With Omicron reportedly having peaked, Hamrick said, “payroll gains should be restored to more solid footing beyond the January report.”

“Even if the nonfarm payrolls report posts a negative read on Friday, it will likely be very reversed in February with a very strong report,” said Scott Ruesterholz, a portfolio manager at Insight Investment.

The labor market remains tight, as evidenced by a low level of initial jobless claims and many job openings, he said. “A drop in January will be noisy data, not a signal that labor market strength is reversing.”

Therefore don’t expect a weak read “to shift the Fed’s game plan for liftoff in March,” Ruesterholz said. “Given noise in data, investors need to look past individual, volatile releases to see the underlying trend.”

Inflation, labor and economic conditions are “consistent with steady Fed tightening.”

Scott Anderson, chief economist at Bank of the West, agreed, ADP’s report “increases the odds of a negative BLS employment report surprise.”

Primary to come:

Rayburn Country Securitization is set to price $908.289 million of senior secured cost recovery bonds, consisting of $205.399 million of Series 2022 Class A-1, term 2032; $353.327 million of Series 2022 Class A-2, term 2043; and $349.623 million of Series 2022 Class A-3, term 2051. Jefferies.

Triborough Bridge And Tunnel Authority (/AA+/AA+/AA+) is set to price $650.915 million of payroll mobility tax senior lien bonds, Series 2022A, serials 2034-2042, terms 2047, 2052 and 2057. Ramirez & Co.

Virginia Small Business Financing Authority (/BBB-/BBB/) is set to price Thursday $627.625 million of tax-exempt/alternative minimum tax senior lien revenue refunding bonds, Series 2022. J.P. Morgan Securities.

The Black Belt Energy Gas District (Baa1//A-/) is set to price $490.78 million of gas project revenue bonds, 2022 Series A. Goldman Sachs & Co.

Tarrant County Cultural Education Facilities Finance Corp., Texas, (Aa3/AA-//) is set to price Thursday $215.68 million of hospital revenue bonds, Series 2022. UBS Financial Services.

Upper Arlington City School District, Ohio, is set to price $125.23 million of unlimited tax general obligation revenue bonds, consisting of $55.71 million of Series A, serials 2032-2037, terms 2040, 2044 and 2048; $64.545 million of Series B, serials 2022-2028, terms 2052 and 2055; $4.975 million of Series A-CAB, serials 2022-2031. Stifel, Nicolaus & Co.

Georgetown Independent School District, Texas, (Aaa/AAA//) is set to price $103.88 million of taxable unlimited tax refunding bonds, Series 2022-A, insured by Permanent School Fund Guarantee Program. FHN Financial Capital Markets.

National Community Renaissance of California (/A+//) is set to price Thursday $100 million of taxable social corporate CUSIP bonds, Series 2022, serial 2032. Morgan Stanley & Co.

Competitive:

Hampton, Virginia, is set to sell $117.37 million of general obligation public improvement bonds, Series 2022A at 10 a.m. eastern Thursday.

Original Source: https://www.bondbuyer.com/news/municipal-long-end-sees-large-gains-over-two-sessions